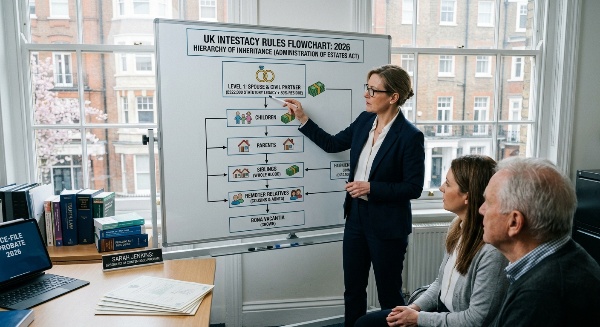

The 2026 Intestacy Rules Flowchart dictates who inherits when there is no Will. This flowchart-based guide explains the hierarchy, from the £322,000 Statutory Legacy for spouses to the final distribution for “remoter” relatives like cousins and the Crown.

Read our complete guide on contesting a will for lack of capacity.

Understanding the 2026 Intestacy Hierarchy

Dying without a Will—known as dying intestate—triggers a strict legal process in England and Wales governed by the Administration of Estates Act 1925. As of 2026, the rules remain rigid, prioritizing the nuclear family before extending to more distant relatives. The primary update for those dealing with estates in 2026 is the Statutory Legacy, which was increased to £322,000 (effective for deaths after July 2023) to reflect inflationary pressures.

The Intestacy Rules Flowchart: Who Inherits What?

The distribution of an intestate estate follows a “branch” system. If a relative exists in a higher branch, they inherit everything, and the branches below them receive nothing.

- Level 1: The Spouse or Civil Partner

If the deceased was married or in a civil partnership and had no children, the spouse inherits the entire estate. If there are children, the spouse receives:

- All personal belongings (chattels).

- The first £322,000 (the Statutory Legacy).

- 50% of the remaining balance (the “residue”).

- Level 2: The Children

The children inherit the other 50% of the residue immediately (or in trust if under 18). If there is no surviving spouse, the children inherit the entire estate equally.

- Level 3: Parents & Siblings

If there is no spouse and no children, the estate moves to the deceased’s parents. If they have passed away, it moves to full-blood siblings (those who share both parents).

The “Remoter” Relatives: From Aunts to Cousins

If no immediate family members are found, the flowchart continues to expand:

- Half-blood siblings (sharing one parent).

- Grandparents.

- Whole-blood aunts and uncles (and their children—the cousins).

- Half-blood aunts and uncles.

The “Common-Law” Myth in 2026

One of the most dangerous misconceptions in 2026 is the idea of a “common-law marriage.” Despite frequent Law Commission proposals, the intestacy rules do not recognize unmarried partners, no matter how long they lived together. If your partner dies without a Will, you could be forced to leave your family home if it was only in their name. To resolve this, many partners must file an Inheritance Act 1975 claim to prove they were financially dependent.

Bona Vacantia: When the Crown Inherits

If a person dies with no surviving blood relatives within the established categories, the entire estate passes to the Crown. This is known as Bona Vacantia (vacant goods). In 2026, the Government’s Treasury Solicitor maintains a public list of these estates, allowing cousins and remoter relatives up to 12 years (or 30 years in some cases) to prove a claim before the money is permanently absorbed by the state.

Partial Intestacy: When a Will Fails

Disputes often arise in 2026 due to partial intestacy. This happens when a Will exists but is poorly drafted and fails to distribute the entire estate. For example, if a Will leaves a house to a friend but doesn’t mention a bank account worth £200,000, that cash is distributed via the intestacy flowchart. Solicitors help resolve disputes in these cases by interpreting the Will alongside the statutory rules.

Inflation and the “Statutory Legacy” Trap

A critical factor in 2026 is the automatic indexation of the Statutory Legacy. Following the 2023 increase to £322,000, the government now reviews this figure every two years in line with the Consumer Price Index (CPI). For families dealing with an intestacy in 2026, this means the fixed “first slice” of the estate going to the spouse is larger than ever.

While this protects the surviving partner, it frequently leaves the deceased’s children—particularly those from previous marriages—with a significantly smaller inheritance than they might have expected. This “inflation trap” is a primary driver of probate disputes in 2026, as children seek to challenge the valuation of estate assets to ensure their 50% share of the residue remains substantial.

The 2026 Bona Vacantia Fraud Safeguards

The Bona Vacantia Unclaimed Estates list underwent a major transformation in early 2026. Following a brief suspension due to concerns over organized criminal groups using the data for fraudulent claims, the Government Legal Department reinstated the list with new “restricted data” protocols. As of April 2026, the public list now only displays the deceased’s name, area of death, and a case reference.

Detailed family history or asset values are now hidden behind a “proof of entitlement” wall. For cousins or distant kin trying to resolve disputes over ownerless property, this makes the initial search more difficult and necessitates the use of forensic genealogists to verify a connection before the Crown will release further details.

Digital Assets and Intestacy: The New Frontier

With the passage of the Property (Digital Assets etc.) Act, 2026 marks the first year that digital holdings like cryptocurrency, NFTs, and monetized social media accounts are formally recognized as personal property in the same category as physical gold or cash. Under the 2026 intestacy rules, these digital assets fall into the “personal chattels” or “residue” categories depending on their nature.

However, because they are often password-protected or held on decentralized exchanges, they frequently go missing. Solicitors now play a vital role in “digital asset tracing”—using court orders to compel tech platforms to grant access to the personal representatives of an intestate estate, preventing thousands of pounds from being lost to the “digital void.”

The 2026 Inheritance Tax (IHT) Impact on Intestacy

Significant IHT reforms taking effect in April 2026 have added a new layer of complexity to intestate estates. While the spousal exemption still applies, the new £1 million cap on 100% Agricultural and Business Property Relief (APR/BPR) means that family farms or businesses worth over £1.325 million (when combined with the nil-rate band) may now face a 20% tax bill for the first time.

In an intestacy, where there is no Will to structure these assets tax-efficiently, the estate may be forced to sell off land or business shares to pay the tax. Solicitors help families navigate these “liquidity crises” by applying for the new 10-year interest-free installment plans offered by HMRC, ensuring the family legacy isn’t dismantled by a lack of planning.

Let’s Do This Together

Contesting a will could become an overwhelming experience if not accompanied by expert guidance and support. Our mission is to provide you with all the needed information, support, and authority to get through this journey, with only one goal in mind: Fairness.

To our team, this process is not about winning; it’s about claiming what was yours from the beginning.

Get your free, no-obligation case assessment. Call 08002980029 or visit contestawilltoday.com

Learn more about our No Win, No Fee service.

FAQs

1. What is the current Statutory Legacy in 2026?

The Statutory Legacy is currently £322,000. This is the fixed sum a surviving spouse or civil partner receives before any remaining assets are split with the children.

2. Can step-children inherit under the flowchart?

No. Step-children have no rights under the intestacy rules unless they were legally adopted by the deceased. To protect step-children, a Will is absolutely necessary.

3. What if I am separated but not yet divorced?

Under the 2026 rules, a separated spouse is still considered a legal spouse until the Final Order (Decree Absolute) is issued. If you die before the divorce is finalized, your estranged spouse could inherit the bulk of your estate under the flowchart.

Meet Our Founder

With over 30 years of experience across civil litigation and dispute resolution, DS Bal brings a deep, broad understanding of the legal process to every case. His background spans complex disputes involving individuals, families, and estates. LinkedIn